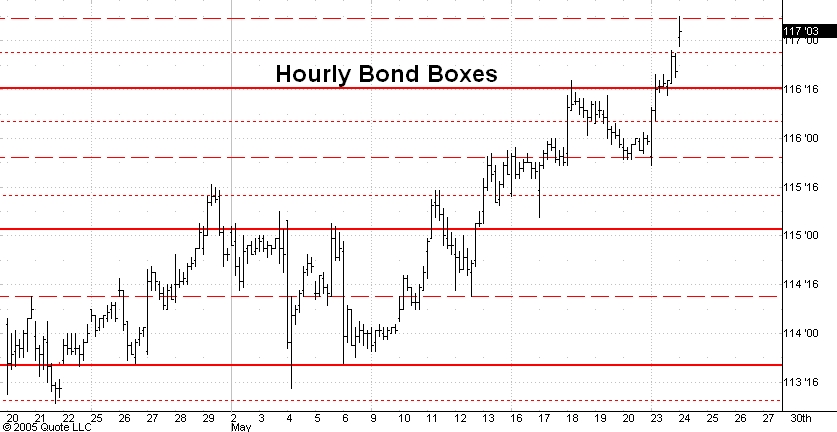

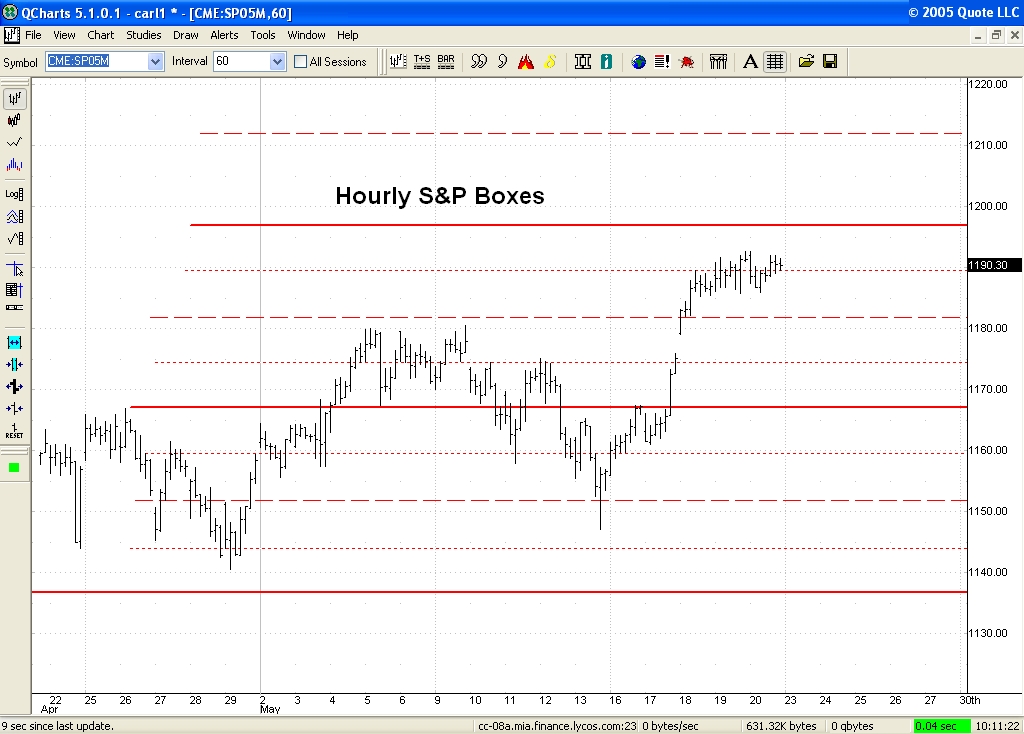

Over the years I have come around to the view that

a good speculator is really an artist. He or she tries to imagine events which haven't yet happened and market conditions and prices which are quite different from those which now prevail. And the speculator hopes to profit from the journey the market will make to a price which at the moment exists only in his imagination.

Like a talented painter or musician, a talented speculator cannot afford to give his imagination completely free rein. Instead his artistic conception of the future arises from a mysterious combination of intuition and technical skill.

The speculator's tools (e.g. charts, computers, market models, etc.) serve to discipline his imagination. These tools guide his insights into channels that have been carved out by historically observed correlations among events.

In the same way a painter's brush technique and use of color allows his artistic muse to express his vision in a way known to be most effective by past generations of painters.

I think that the amateur speculator's

biggest problem is a lack of imagination,

not a lack of tools. This problem usually shows up in his very short term outlook on markets. I belong to a number of market discussion groups and am always struck by the focus on what will happen tomorrow or next week as opposed to what the market's trend will be over the next six months or a year.

Why this extremely short term focus? Well, one reason is the ease with which people nowadays can track markets tick by tick. Only 25 years ago it was very expensive to monitor markets during trading hours so most people had to content themselves with knowing the daily high-low-close. Markets seemed then to move at a slower pace (only an illusion of course!).

But I think there is a second reason for this short term focus, a reason which reflects a fundamental misunderstanding of the way markets move. Amateur speculators seem to think that price changes are somehow more predictable over short time frames than over long time frames.

From a statistical point of view this belief is complete

nonsense. In fact the volatility of price changes (measured by the standard deviation, for example)

decreases as the length of time over which the price change is measured

increases. Put another way,

price changes are much more random in the very short run than they are in the long run!

I believe that it is

much harder to forecast what the market will do today or tomorrow than it its to forecast what it will do over the next year! Moreover, even if you want to profit from short term price fluctuations, it is much easier to do this if you have a reliable estimate of what the market will be doing over a longer time frame, one which will include several of your shorter term trades.

So pick your forecasting methods so that they give you as much information as possible about the market's longer term trend. If you get this right it is much, much easier to take advantage of the short term price fluctuations which occur as the market progresses towards your more certain longer term target.